Transformation of the Payments Industry: 2025 Round Up

Transformation of the Payments Industry: 2025 Round Up

The consumer really is king when it comes to the payments industry.

It would be hard to disagree, given the change of pace over the past five years.

Consumers want to bank without banks; pay without cash, or PIN numbers; use ‘one-click’ checkouts securing, transfer money abroad with ease; all whilst feeling secure and protected. Traditional banks and payment providers are facing new challenges, alongside a stricter post-recession regulatory environment.

Trends Shaping the Payments Industry

We believe the following seven trends will continue to transform the industry, based on our experience across a wide range of sectors and countries, and the our constantly innovating digital world

- Mobile and Contactless Payments

- Financial Services for the Unbanked

- Digital Giants

- Security Concerns

- Fintech M&A / Market Consolidation

- Increase Regulatory Control

- Faster payments

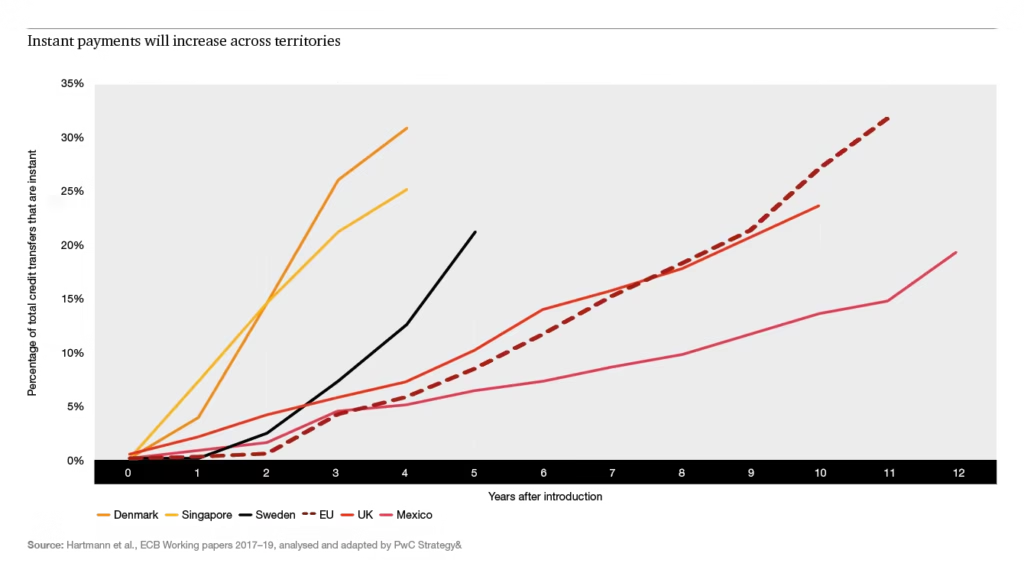

Mobile Payments and Contactless Payments

Global mCommerce payments volumes are on a steady upwards trajectory. Only five years ago this figure was £33 billion, at current exchange rates. In 2015, they are set to hit £281 billion, with £720 billion predicted in 2017. Consequently, mobile payment technology is adapting to meet consumer demands.

There are three factors driving this: a consumer-led move to mobile shopping, the adoption of Near Field Communication (NFC) as a payment method and m-commerce apps that can be used in retail outlets.

With NFC enabled on more cards and devices (including Apple Pay) than ever before, cash could be nearly obsolete in ten years.

Major retailers, such as Starbucks, now have apps that include a payment feature, allowing customers to click and collect, or pay in store using their app (via NFC-enabled smartphones). Where Apple and Starbucks lead, others will follow.

Financial Services for the Unbanked

The financial services sector is off limits for 2.5 billion people around the world. Financial exclusion makes it that much harder to achieve economic empowerment, with many commercial and charitable organisations looking to implement solutions using technology.

A Gates Foundation and McKinsey & Company study found that mobile payments and m-Banking would reduce transaction costs for the poor by 9o percent. Services such as M-Pesa, from Kenya (available in Eastern Europe since 2014) already offer mobile credit, banking and savings. Given the size of this market, we expect this trend to keep shaping the industry for decades.

Digital Giants

Google, Facebook, Twitter, Amazon and Apple pose a significant threat to traditional banking, according to BNY Mellon report(.pdf). In 2014, total social commerce sales that could be tracked to social networks hit $3.30 billion, up 26% from 2013’s $2.62 billion – Internet Retailer’s “2015 Social Media 500”, a study of 500 leading merchants’ use of social media.

It’s therefore no surprise that these social media and digital giants with their huge user-bases are looking for ways to enter the payments industry, potentially cutting into banks and other providers markets.

Security Concerns

At the same time, customers and regulators are increasingly concerned about security. Data breaches are more common. Hundreds of millions of identities and payment details have been extracted from banks, technology firms and retailers over the last few years.

Hackers and criminal gangs buy and sell this data. It is proving to be an evolutionary war, between the industry and criminals. Fortunately technology such as tokenisation is increasingly being deployed to keep payment card data safe. This process ensures that returning customers using ‘one-click’ checkout services do not need to key in payment card details every time they make a purchase – keeping their data safe and out of reach.

Fintech M&A / Market Consolidation

Banks are keeping a close eye on emerging players in the payments and financial sector. It should be no surprise that the largest concentration of financial tech (fintech) startups is in London, England.

London is the birthplace of the financial sector, occasionally the centre of the industry, when New York falls to second place.

CB Insights found that fintech investment is currently growing at three times the rate of VC funding, with £8.2 billion in 2014. The bulk of the £417 million invested in the UK went to London. Julian Skan, Accenture managing director banking in Europe, Latin America and Africa said “The massive investment in fintech shows that the digital revolution is well advanced in financial services, and it is both a threat and an opportunity for banks.”

Expect consolidation, with banks buying early and growth stage startups, as industry leaders prove their value to consumers and businesses alike.

Summary:

- • Once a quiet corner of financial services, now an active and innovative industry, payments are undergoing a transformation,

- • Consumer demand is being driven by new technology, created to meet demand: this cycle will accelerate to drive innovation,

- • MCommerce, contactless payments, mobile transfers and banking are a huge growth market, set to disrupt cash, international payments and banking,

- • New technology must maintain rigorous security standards. Otherwise customers will soon lose trust,

- • We expect a land grab throughout the payments industry, as larger players benefit from early-stage innovations.

{kind=link}